The 6th April 2020 began a new tax year and with it came a new batch of allowances and reliefs which provide useful opportunities to save or claim money, however in many cases, if not used these will be lost from one tax year to the next. This includes ISA, Pension and annual exempt gifts.

As a result of ‘social distancing’ nearly everyone now finds themselves with more time on their hands. Cupboards have been tidied, rooms painted, and gardens well tended but one area which may remain neglected is our finances. In this article we share some simple ideas, which we believe can help individuals and families get their finances in order and plan more effectively for the future.

The 6th April 2020 began a new tax year and with it came a new batch of allowances and reliefs which provide useful opportunities to save or claim money, however in many cases, if not used these will be lost from one tax year to the next. This includes ISA, Pension and annual exempt gifts.

Creating a plan

When thinking about your finances do you have specific goals in mind? Often these depend on what stage of life you are at and can change over time as your income, overall wealth and circumstances change. Before looking at specific ideas it is important to consider their purpose and how they fit within a wider plan, as looking at these things out of context or in isolation can be likened to re-arranging the deck chairs on the Titanic before it sank.

It can be difficult to do this on your own without any sort of guidance, however a discussion with an experienced financial planner can help you to set short, medium and long term objectives and create a structured plan, tailored to your circumstance, to help achieve these.

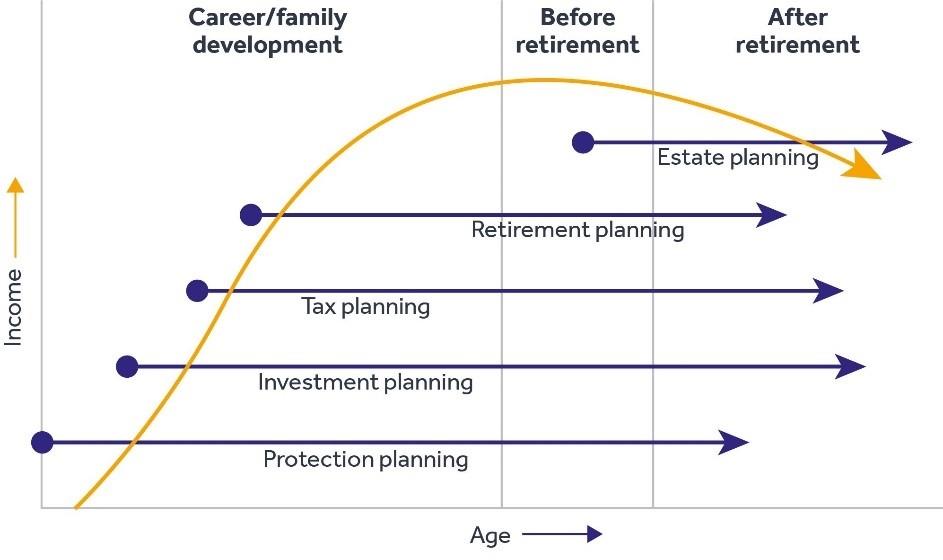

As mentioned, your objectives will depend on what stage of life you are at. There are broadly 3 main life stages which everyone will go through;

- Career / Family development

- Before retirement

- After retirement

At each stage your focus and priorities may change as shown in the graph below, but our aim is to build lasting relationships with our clients and their families to help successfully navigate each stage and provide successful outcomes for them.

Life stages

Turning then to some specific ideas to consider in this new tax year.

1.Investment planning – avoiding mistakes and seizing opportunity

One of many unfortunate outcomes of the current crisis is that financial markets, which ultimately determine the value of many investments and pensions, have suffered from some sharp short-term falls.

Whilst this can be unsettling for those with money invested, historical data available to us would suggest that given time, markets will recover. For those with well researched and diversified portfolios the best advice in nearly every case will be to remain invested, however it can be worthwhile arranging a review of your current investment strategy to ensure its suitability.

For those thinking about adding to existing investments or commencing investment then this could be a once in a lifetime opportunity to capture low investment values and benefit from a market recovery whenever this occurs and boost long term returns.

Some of the allowances and reliefs described below can be used to offset losses whilst effective financial planning can ensure that measures are taken which help mitigate some of the risk of investing.

2. ISA Allowance

The ISA allowance for 2020/21 remains unchanged at £20,000 for each individual, however the Junior ISA (JISA) allowance has nearly doubled, offering the opportunity to save for children or grandchildren in a tax efficient manner. The new JISA allowance is now £9,000 per child. For those with children aged 16 and 17, they can use the JISA allowance of £9,000 and also the £20,000 allowance for a cash ISA.

There are a variety of ISA’s available depending on your objective and appetite for investment risk which can be tailored to your circumstances and goals.

3. Pensions – Savings

Pensions remain the most effective means of saving for retirement due to the tax relief available on all personal contributions. This tax relief is typically available at your highest rate of income tax but both this and the maximum amount that you can contribute to your pension are determined by your overall income. The Tapered Annual Allowance which reduces the amount higher earners can put into a pension tax efficiently has increased to starting at income above £200,000, more information on this can be found here. This can be a complex area and if you would like explore this in more detail then please arrange to speak to an adviser.

As with Junior ISA’s, described above, pensions can also be used as a means of providing long term savings for children from birth. Relatively modest contributions now can have a huge impact on a child’s future pension savings without some of the worries of a JISA when money is at their disposal from age 18.

4. Building cash reserves

Often neglected is the need to have cash available for those ‘rainy days’ or emergencies. This has never been more apparent than now, as were it not for a series of government support packages many would find themselves without work and income leaving them in a precarious financial position. Starting to put money aside now can serve to take the pressure off when the next crisis comes along and ease some of the worries this could create.

For many, not travelling to and from work coupled with other savings in their normal expenditure as a result of being locked down can mean that they are actually better off financially at the moment. Rather than spending all these savings on Amazon this could be the perfect opportunity to start putting money aside and create a good lifelong savings habit.

5.Taking action

Hopefully these points provide some useful food for thought and inspire you to carry out a ‘spring clean’ of your financial arrangements. If you would like some assistance or would simply like to discuss these points in more detail then please get in touch.

To find out more about our Services please contact our team today on T. +44 (0) 28 9032 9042 or fill out the form below: