With major stock markets worldwide now going into a Bear Market (NASDAQ, S&P 500, FTSE 250 already and Dow Jones close), we look at what this is and historically the best way to get through this uncomfortable time for investors. A bear market is typically defined as a 20% drop from recent highs. The most common usage of the term is to refer to the S&P 500’s performance, which is generally considered a benchmark indicator of the entire stock market.

Bear markets are quite common. Since 1900, there have been 33 of them, so they occur every 3.6 years on average and last an average of 8.8 months . Just to name the three most recent notable examples:

- 2000-2002 dot-com crash: Growing use of the internet in the late 1990s led to a massive speculative bubble in technology stocks. While all major indices fell into bear market territory after the bubble burst, the Nasdaq was hit especially hard: By late 2002, it had fallen by about 75% from its previous highs.

- 2008-2009 financial crisis: Due to a wave of subprime mortgage lending and the subsequent packaging of these loans into investable securities, a financial crisis spread across the globe in 2008. Many banks failed, and massive bailouts were required to prevent the U.S. banking system from collapsing. By its March 2009 lows, the S&P 500 had fallen by more than 50% from its previous highs.

- 2020 COVID-19 crash: The 2020 bear market was triggered by the COVID-19 pandemic spreading across the world and causing economic shutdowns in most developed countries, including the U.S. Because of the speed at which economic uncertainty spread, the stock market’s plunge into a bear market in early 2020 was the most rapid in history.

Even with 3 Bear Markets (2008, COVID and Now) in the last 20 years, if you invested £1,000 into a market tracker and did not take any money out then your money would be worth between £3,103.13 if invested in the FTSE 100 and £13,772.73 if invested in the NASDAQ 100 today.

Back to “How to survive a Bear Market”:

- Your Investment Strategy is Long Term – Most clients have a long term investment objective. Even those approaching retirement will likely be invested for 30+ years. Historical returns show that investing is stocks and shares over the long term has historically always beat savings and inflation over a 10 year period. Our clients will have diversified portfolios that are invested for long term capital growth above inflation. Although we must take notice of shorter term problems, this should not mean a complete shift in investment principles. The average investor significantly underperforms the overall stock market over the long run, and the primary reason is moving in and out of stock positions too quickly. When stocks plunge and seem as if they’ll keep falling forever, it’s our instinct to sell “before things get any worse.” Then, when bull markets happen and stocks keep reaching new highs, we put our money in for fear of missing out on gains.

- Don’t try to “Time the Market” – Trying to time the market is generally a losing battle. There have been many finance papers on this and some of the smarted people in finance have not been able to do it. One thing to keep in mind during bear markets is that you aren’t going to invest at the bottom. Buy stocks because you want to own the business for the long term, even if the share price goes down a little more after you buy. The average S&P 500 bull market is 178% and lasts 60 months. This is over four times larger and longer than the average bear market drops of -38% over 19 months. So, history tells us that the markets reward investors who dig their heels in and ride out the tough times.

- Diversification & Emergency Funds – All investors should keep an amount of Emergency Cash Deposits that will allow peace of mind to be able to take less or stop taking income or capital from their portfolios. As well as this our diversification strategy means that we will have invested in different equites, bonds and sectors and although the current climate has seen the majority of sectors and asset classes falling in value, we have the below element of your portfolio that have increased in value over the last year and immediate monies could be taken from these assets while we wait on a recovery:

- A Paper Loss is not an actual Loss until it is realised – Although bear markets are uncomfortable and nerve wracking, they are not actually losses until they are sold. For the majority of investors the time frame for these investments is further down the line and historically if you can wait 12 – 18 months, you have a good chance to never actually suffer an actual loss. As we have mentioned above our portfolios have some funds that have continued to thrive in current conditions and clients should be taking any capital or income needs from these assets if they can to not capitalise a loss on the funds that are currently suffering the brunt of the bear market.

- Analyze your current holdings to see if they are still correctly invested for the future – We have spent hundreds of hours over the last 6 months, trying to make sure our portfolio still have the correct mix for our clients to attain their objectives. We have a slight bias in the portfolio to “quality” companies whether this is in the “growth” or “value” space. Investing in quality companies is rooted in a thorough fundamental analysis of all aspects of a company’s financial strength, growth prospects, profit and income generation and overall stability.

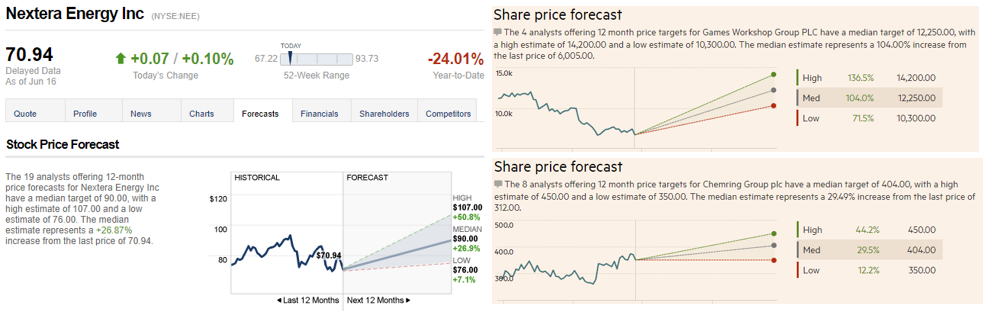

Below we look at 9 of the top US stocks in the portfolio and 2 in the UK. Between them they make up less than 5% of most portfolio but shows a snapshot of current conditions and analyst predictions for next 12 months. The US data is supplied by CNN and the UK data by Financial Times.

Performance of Major Indices since 2006

Please see the below table up to June 16th 2022 showing the annual performance of a few of the major indices and the value of £1,000 invested in each of these 10 or 20 years ago. As you can see there are periods of negative growth throughout each of the indices but if you invested in the S&P 500 or the FTSE 250 10 years ago and held your money then you would have had an average annual return of 15.53% and 8.49% respectively. (This included the recent bear market).

Summary

As you can see from the above, stock markets do move up and down and due to this, it is important to always make sure your appetite for risk is correct. Investing over the long term can be difficult as you will have periods of negative growth and large swings in value but historically this has been rewarded for investors who are able to stay invested as the above tables show.

It is important to always review your level of risk and make sure these are still suitable for your objectives.

Past performance is not a guide to future performance, nor a reliable indicator of future results or performance. The value of your investment can go down as well as up, and you can get back less than you originally invested.

For more information please contact Stephen Willis on stephenw@willisfinancialservices.co.uk

To find out more about our Services please contact our team today on T. +44 (0) 28 9032 9042 or fill out the form below: